Secure Your Future with Confidence: Discover the Power of Indexed Annuities

- Ling Zhang

- Jun 6, 2025

- 3 min read

Your Bridge to a Stress-Free Retirement: Indexed Annuities Explained

When it comes to planning for retirement, many people face a daunting question:

“How can I grow my money without risking it all in the market?”

If you’ve been saving, investing, or even watching from the sidelines as market swings threaten your hard-earned dollars, you’re not alone. The good news? There’s a retirement strategy that blends growth potential, principal protection, and lifetime income—it’s called an Indexed Annuity.

🌱 What is an Indexed Annuity?

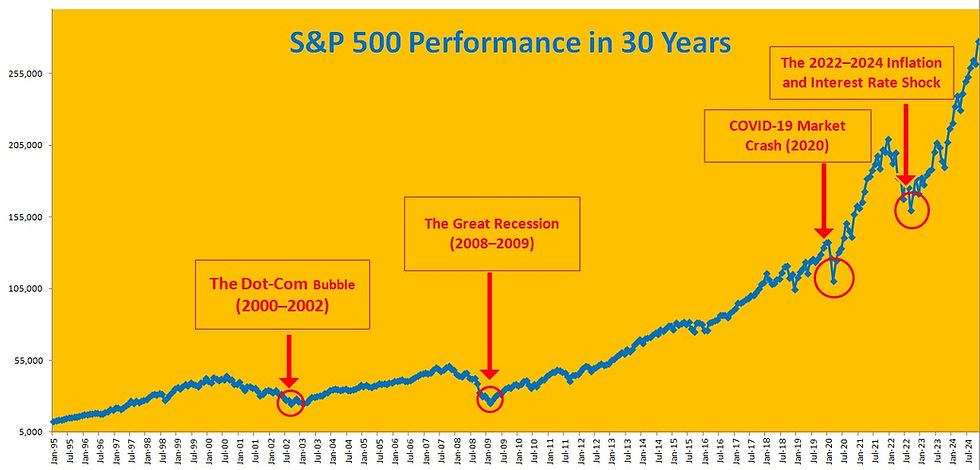

An indexed annuity is a type of insurance product that allows your money to grow based on the performance of a stock market index (like the S&P 500), while also protecting your principal from loss when the market declines.

It has two main phases:

Accumulation Phase: Your money earns interest linked to a market index, typically 3%-6% average annually, with zero market losses.

Distribution Phase: When you retire and need to draw income, the annuity pays out based on a protected value (5%-8% growth rate), often for life.

💡 Why People Choose Indexed Annuities

Imagine you’re climbing a mountain. Indexed annuities are like climbing with a safety harness—you can still go up when the weather is good (market rises), but you’re protected from falling when the weather turns.

Here’s what makes them shine:

✅ Principal protection: Your original investment is shielded from market losses.

✅ Tax-deferred growth: Earnings compound without yearly taxes until you withdraw.

✅ Market-linked growth: Enjoy part of the upside without risking the downside.

✅ Guaranteed lifetime income: You won’t outlive your money.

✅ Sign-on bonuses & fixed growth riders: Many products offer immediate boosts and steady gains even in flat markets.

👥 Who Are Indexed Annuities Best For?

Indexed annuities are ideal for:

🔹 Pre-retirees (age 50+): Looking to grow wealth safely while avoiding volatility.

🔹 Retirees: Seeking guaranteed income and peace of mind.

🔹 Conservative investors: Who want better returns than CDs or bonds without market risk.

🔹 Those with rollover funds: Such as 401(k), IRA, or large savings accounts needing better allocation.

🤔 “But Aren’t Annuities Too Complex or Expensive?”

That’s a common concern—and one worth addressing.

Concerns 1: “I heard annuities have high fees.”

✔️ Reality: Indexed annuities typically have low or no annual fees, unless you add income riders (which bring extra value).

Concerns 2: “What if I need to access my money?”

✔️ Reality: Most indexed annuities offer 10% free annual withdrawals and penalty-free income after the surrender period.

Concerns 3: “Isn’t the stock market better long-term?”

✔️ Reality: Possibly—if you’re okay with risk. But if retirement is near, indexed annuities offer peace of mind, predictability, and income you won’t outlive.

📈 Real-World Example

Consider a 65-year-old retiring with $1 million:

With an indexed annuity, the annuity value grows with time.

By retirement, the payout could be $50,000/year for life, with zero market risk.

Even if the market drops 20%, your income stays steady—because your payout value never goes backward.

✨ Final Thoughts: Dare to Grow—Safely

In a world full of economic uncertainty, indexed annuities offer a beautiful balance of protection and potential. It’s not just about making more money—it’s about making sure your money lasts.

If you're tired of watching the market with worry or unsure if you’ll have enough to retire, an indexed annuity might just be the financial foundation you've been searching for.

If you’d like to learn how to build a diversified financial strategy tailored to your goals, 👉 Learn the three cornerstones of building wealth

May you grow to your fullest!

Subscribe Grow to Your Fullest for Financial Tips

*** Please DOWLOAD the FREE document, Find your signature vision questionnaires so you use it to help you find your life vision and mission.

>> Contact Grow to Your Fullest

Comments